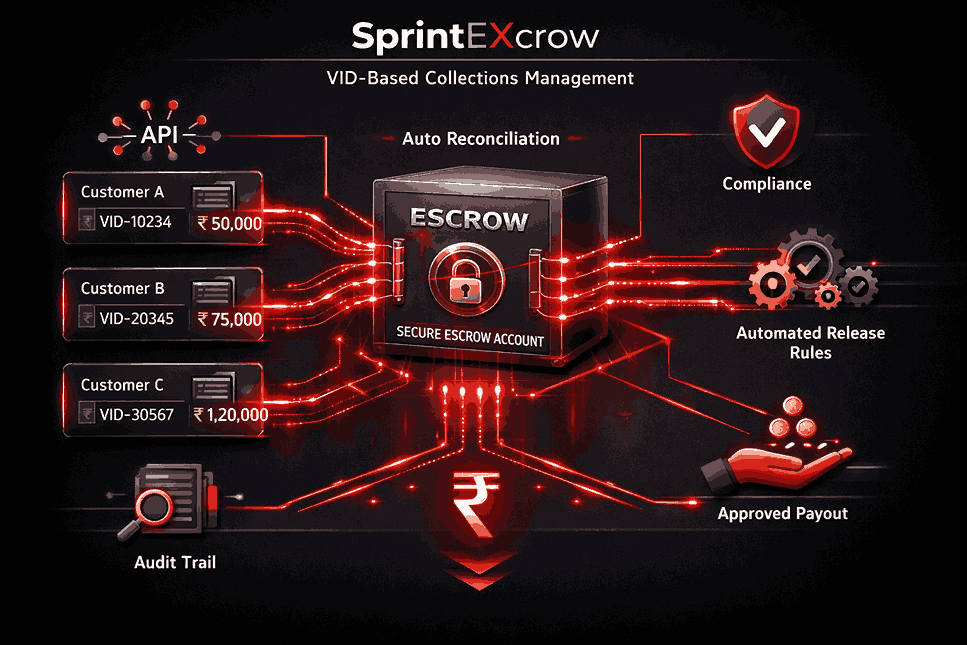

VID Collection refers to the transaction that collects the amount in the escrow account via a Virtual ID, enabling seamless, trackable fund inflows without sharing full bank details. In high-value escrow transactions, this method ensures precise reconciliation by assigning unique Virtual IDs to each deal, eliminating commingling risks. SprintEXcrow by PaySprint leverages VID collection to power secure pay-ins for real estate, B2B contracts, and marketplaces, making fund custody automated and compliant.

Table of Contents

What Is VID Collection in Escrow?

Why VID Collection Matters for Businesses

How SprintEXcrow Handles VID Collection

Step-by-Step VID Collection Process

Key Benefits for Reconciliation and Compliance

Industry Use Cases

Integration and Onboarding

Conclusion

Frequently Asked Questions

What Is VID Collection in Escrow?

VID Collection uses Virtual Account IDs (or Virtual IDs) linked to a master escrow account, allowing buyers to deposit funds directly while auto-matching payments to specific transactions. Unlike pooled collections, each VID acts as a segregated identifier, ensuring one-to-one reconciliation between pay-ins and escrow ledgers. SprintEXcrow generates these VIDs via API, providing instant confirmation and dashboard visibility for trustees, buyers, and sellers.

For businesses operating in digital ecosystems, VID-based escrow aligns seamlessly with secure escrow in embedded finance models where API-driven transactions are critical.

Why VID Collection Matters for Businesses

Traditional collections mix funds across transactions, creating reconciliation nightmares with manual matching across bank statements. VID Collection solves this by provisioning unique IDs per escrow deal, guaranteeing traceability from deposit to release. For PaySprint's SprintEXcrow users, this means faster audits, reduced disputes, and RBI-compliant nodal management in COD-heavy or multi-party flows.

Common challenges it addresses:

Fund misallocation in high-volume escrow.

Delayed pay-in verification.

Compliance risks in pooled accounts.

How SprintEXcrow Handles VID Collection

SprintEXcrow integrates with partner banks to dynamically create Virtual IDs tied to escrow sub-accounts, supporting UPI, netbanking, and cards. Funds hitting the VID instantly reflect in the platform's unified ledger, triggering automated status updates (e.g., "Funds in Escrow").[conversation_history] The dashboard provides real-time MIS reports, easing reconciliation with transaction references like order IDs or milestones.

Step-by-Step VID Collection Process

Initiate Escrow: Create transaction via SprintEXcrow API, generating unique VID.

Share VID Details: Send VID, amount, and expiry to buyer via link, QR, or invoice.

Buyer Deposits: Funds transfer to VID-mapped escrow account.

Auto-Reconciliation: Platform matches deposit to transaction; notifies parties.

Hold & Release: Funds held until conditions met; seamless payout on approval.

Key Benefits for Reconciliation and Compliance

SprintEXcrow's VID Collection cuts reconciliation time from days to minutes through auto-matching and audit trails. Businesses gain:

100% Segregation: No fund mixing; each VID = one transaction.

Real-Time Tracking: Dashboard shows VID status, balances, and disputes.

RBI Compliance: Nodal/escrow adherence with KYC-verified flows.

Scalable APIs: Embed VID collection in apps for zero manual intervention

To understand trade finance differences, businesses can explore escrow vs letter of credit for a structured comparison of risk allocation and usage scenarios.

Industry Use Cases

Real Estate: Buyers send deposits via VID; auto-match to property deals

Marketplaces: Per-order VIDs for vendor payouts. This mirrors structured escrow in eCommerce frameworks designed for secure buyer-seller settlements.

Freelance/B2B: Milestone payments collected securely. Growing companies increasingly rely on escrow for startups to strengthen partner and investor trust.

COD E-commerce: Bridge offline collections with digital escrow. International sellers can also leverage cross-border payments with escrow to ensure transparent fund custody across geographies.

Integration and Onboarding

Integrate SprintEXcrow APIs in hours: onboard via PaySprint, configure VID rules, and test live flows. Support includes custom MIS for VID reconciliation and multi-bank routing.

Businesses can also evaluate the difference between money escrow and software escrow to choose the right protection model for their transactions.

Conclusion

VID Collection transforms escrow pay-ins into a frictionless, reconciled process, powering SprintEXcrow's promise of trust at scale. Businesses handling high-value transactions gain speed, security, and compliance, turning Virtual IDs into a competitive edge for growth.

Frequently Asked Questions

1. What exactly is a Virtual ID in SprintEXcrow?

A Virtual ID is a unique identifier linked to an escrow sub-account for collecting funds, ensuring automatic matching without sharing core account details.

2. How does VID Collection improve reconciliation?

It enables one-to-one auto-matching of deposits to transactions, providing instant ledger updates and MIS reports.

3. Is KYC required for VID Collection?

KYC applies at the master account level; end-users pay via standard methods without additional verification.

4. Which payment modes support VID Collection?

UPI, netbanking, cards, and IMPS—all routed to the VID for seamless escrow entry.

5. Can SprintEXcrow handle high-volume VID Collections?

Yes, API-driven scaling supports thousands of VIDs daily with real-time dashboards.