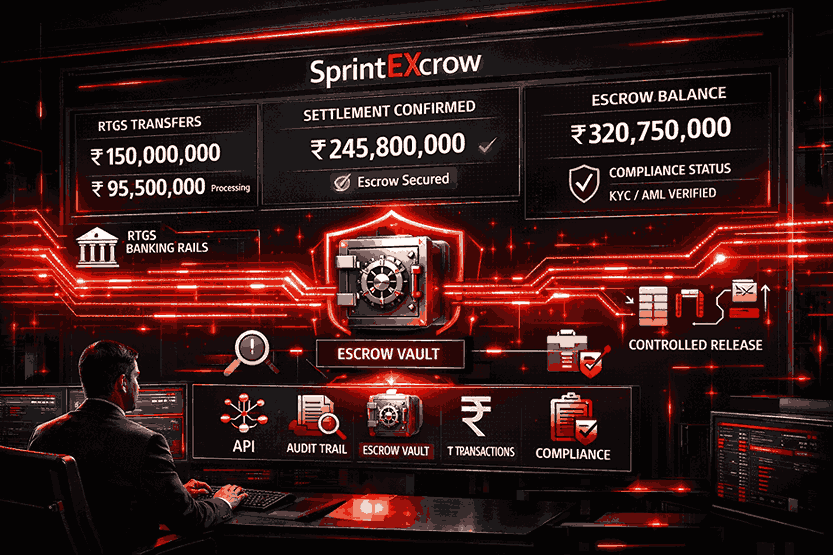

RTGS (Real Time Gross Settlement) is an electronic fund transfer system where money moves from bank to bank in real-time, individually for each transaction, without waiting for other transactions to clear, making it ideal for large-value, time-sensitive payments in India and globally. In escrow workflows, RTGS powers instant, high-amount pay-ins and payouts through SprintEXcrow, ensuring secure custody and immediate ledger reconciliation for deals exceeding ?2 lakhs.PaySprint's platform integrates RTGS seamlessly for real estate, enterprise contracts, and B2B transactions requiring bank-grade certainty.

Table of Contents

What Is RTGS in Escrow Transactions?

When RTGS Outshines Other Payment Rails

SprintEXcrow's RTGS Capabilities

RTGS Collection and Payout Process

Strategic Benefits for Large Transactions

Industry Use Cases

Limits, Timings, and Compliance

Conclusion

Frequently Asked Questions

What Is RTGS in Escrow Transactions?

RTGS processes each transfer individually and gross (no netting), with funds debiting the sender's account and crediting the recipient's escrow account within seconds during operational hours. Unlike IMPS (smaller amounts) or NEFT (batched), RTGS guarantees finality—no reversals—making it perfect for irrevocable escrow deposits over ?2 lakhs. SprintEXcrow maps RTGS transactions to specific deals via UTR references, enabling instant status updates from "Initiated" to "Funds Secured".

For businesses comparing structured settlement mechanisms, understanding escrow vs letter of credit helps clarify differences in risk allocation and payment finality.

When RTGS Outshines Other Payment Rails

Businesses choose RTGS when transaction values exceed IMPS limits (?5 lakhs) or require settlement finality for compliance-heavy deals. It eliminates batching delays (NEFT) and weekend gaps, critical for time-bound escrow releases like property handovers or milestone completions. SprintEXcrow users leverage RTGS for VID collections and bulk payouts, combining speed with full audit trails.

Key scenarios:

Payments above ?2 lakhs need immediate crediting.

Legal/contractual requirements for irreversible transfers.

Multi-bank flows requiring UTR traceability.

High-value digital transactions increasingly rely on escrow in embedded finance to ensure secure, API-driven fund custody and reconciliation.

SprintEXcrow's RTGS Capabilities

SprintEXcrow exposes RTGS via PayIn/PayOut APIs, generating beneficiary details or payment mandates linked to escrow sub-accounts. Incoming RTGS triggers automated reconciliation against transaction IDs, with dashboard views showing real-time balances and settlement proofs. Partnered with scheduled commercial banks, it supports unlimited high-value RTGS across public/private sectors.

RTGS Collection and Payout Process

Transaction Setup: Create escrow deal; SprintEXcrow provides RTGS beneficiary details (account, IFSC, UTR reference).

Buyer/Sender Initiates: Use netbanking/corporate banking; enter exact amount and reference.

Real-Time Settlement: NPCI/RBI infrastructure credits escrow instantly (within 30 seconds).

Auto-Reconciliation: Platform matches UTR to deal; notifies all parties.

Payout on Conditions: Release via RTGS to the seller on approval.

Strategic Benefits for Large Transactions

RTGS elevates SprintEXcrow for enterprise-grade escrow:

Irrevocable Finality: No chargebacks or reversals post-settlement.

High Limits: No upper cap (unlike IMPS ?5L); handles crores seamlessly.

Operational Hours: 7x12 (Mon-Sat 7 am-7 pm, extended Sundays).

Precise Reconciliation: UTR-based auto-matching cuts manual effort 90%.

Cost Efficiency: Flat fees scale better for large amounts.

Enterprises evaluating long-term protection models should also explore the distinction between money escrow and software escrow for safeguarding both financial and digital assets.

Industry Use Cases

Structured settlements in property transactions often align with escrow for startups and growing real estate ventures seeking investor trust.

Real Estate: Full property payments or developer milestones via RTGS.

Enterprise B2B: Supplier contracts exceeding ?10 lakhs secured in escrow.

M&A/Private Equity: Deal consideration held until closing conditions met.

Infrastructure Projects: Stage-wise funding with RTGS traceability.

Limits, Timings, and Compliance

Minimum ?2 lakhs per transaction; operates Mon-Sat 7 am-7 pm IST (some banks extend). SprintEXcrow ensures RBI escrow guidelines via segregated nodal accounts and KYC-verified endpoints. Failed RTGS auto-handles retries; UTR logs support audits.

Before implementing RTGS-based escrow workflows, reviewing common escrow service myths can help clarify misconceptions around fund control and compliance obligations.

Conclusion

RTGS transforms SprintEXcrow into a powerhouse for large-value escrow, delivering real-time settlement finality that accelerates deals while simplifying reconciliation. From real estate closings to enterprise payouts, businesses unlock liquidity and trust at scale through this robust rail.

Frequently Asked Questions

1. Why use RTGS over IMPS for SprintEXcrow?

RTGS handles unlimited high-value transfers with settlement finality; ideal when exceeding IMPS ?5L limit or needing irrevocability.

2. What are RTGS operational hours?

7am-7pm Mon-Sat (extended Sunday windows at select banks); real-time processing within operational period.

3. How does SprintEXcrow reconcile RTGS payments?

Via UTR references auto-matched to escrow transactions, providing instant ledger updates and MIS reports.

4. Is there a minimum amount for RTGS in escrow?

Yes, ?2 lakhs minimum; perfectly aligns with high-value SprintEXcrow use cases.

5. Can RTGS payouts be scheduled in SprintEXcrow?

Yes, condition-based releases trigger instant RTGS payouts upon milestone verification.