Why Insurance Claim Settlements Need Escrow : Protecting Policyholders and Insurers Alike

Insurance exists to convert uncertainty into assurance — to give policyholders the confidence that when something goes wrong, they will be made whole. The premium is paid. The policy is signed. The promise is made. And then, when a claim is filed, the process that was supposed to deliver on that promise becomes one of the most contested, delayed, and distrusted interactions in financial services.

Claim settlements in India face a structural problem that no amount of process improvement has fully solved: the point at which money changes hands between insurer and policyholder is also the point at which trust most frequently breaks down. Disputed quantum, delayed releases, funds routed to the wrong party, payments made before repairs are verified — these are not edge cases. They are endemic to how claim settlements currently work.

For policyholders, the result is settlements that arrive late, short, or not at all. For insurers, it is fraud exposure, disputed disbursements, and regulatory scrutiny. For the insurance ecosystem as a whole, it is a trust deficit that suppresses both penetration and retention.

SprintEXcrow by PaySprint introduces a neutral, conditional payment layer into the insurance claim settlement process — holding approved claim amounts in escrow and releasing them only when defined conditions are verified. For policyholders, it means certainty that an approved settlement will be paid in full and on time. For insurers, it means control, auditability, and fraud protection at every disbursement.

Table of Contents

1. Why Do Insurance Claim Settlements Go Wrong?

2. What Are the Most Common Insurance Settlement Failures?

3. What Is Escrow and How Does It Apply to Insurance Claims?

4. How SprintEXcrow Works for Insurance Claim Settlement

5. Who Benefits — Policyholders, Insurers, and TPAs?

6. Where Insurance Escrow Matters Most: Key Use Cases

7. Why SprintEXcrow Is Built for Indian Insurance Settlement

8. Conclusion

9. Frequently Asked Questions (FAQs)

Why Do Insurance Claim Settlements Go Wrong?

The insurance claim settlement process involves multiple parties — the policyholder, the insurer, surveyors, third-party administrators (TPAs), repair vendors, hospitals, and sometimes legal counsel. Each handoff between parties is a point of potential failure.

At the core of the problem is the same asymmetry that exists in every financial transaction where payment precedes or follows performance: one party holds the money while the other has already performed, or vice versa. In insurance:

• The insurer approves a claim quantum but has no guarantee the funds reach the right party

• The policyholder receives a disbursement before repair or treatment is completed, with no mechanism ensuring funds are applied to the insured purpose

• Third-party vendors — hospitals, garages, contractors — complete work on the expectation of reimbursement, with no certainty of when or how much they will receive

• TPAs handle disbursements across thousands of claims simultaneously, with manual processes that create reconciliation gaps and fraud exposure

The result is a settlement process where everybody is waiting for somebody else to move, and nobody has structural assurance that the money will land correctly.

What Are the Most Common Insurance Settlement Failures?

Understanding where settlements fail is the foundation for understanding why escrow addresses them so directly.

Delayed Disbursement

Approved claims sit in payment queues for days or weeks. Policyholders who need funds urgently — for medical treatment, vehicle repair, property restoration — are left waiting after the claim has already been approved. The bottleneck is not assessment; it is release.

Diversion of Settlement Funds

Claim amounts disbursed directly to policyholders are sometimes applied to purposes other than the insured loss — genuinely or fraudulently. A motor claim payment that was meant to fund panel beating is used for something else entirely, and the vehicle goes unrepaired.

Underpayment and Partial Settlement

Policyholders receive partial settlements without clear communication of why the full approved quantum is being withheld or phased. Without a structured escrow framework, there is no transparent, auditable record of what was approved, what was released, and what remains pending.

Fraud at the Vendor Level

Hospitals, garages, and contractors inflate invoices or claim for services not rendered, knowing that insurer-to-vendor payment flows are difficult to audit in real time. Without condition-based payment release, there is no mechanism to verify that the invoiced service has actually been delivered before funds are released.

Disputed Quantum at the Point of Payment

Even after a claim is assessed, disputes arise at the payment stage about the final amount. Without a neutral holding mechanism, both parties are negotiating while the funds sit in the insurer’s account — creating adversarial dynamics that delay resolution.

What Is Escrow and How Does It Apply to Insurance Claims?

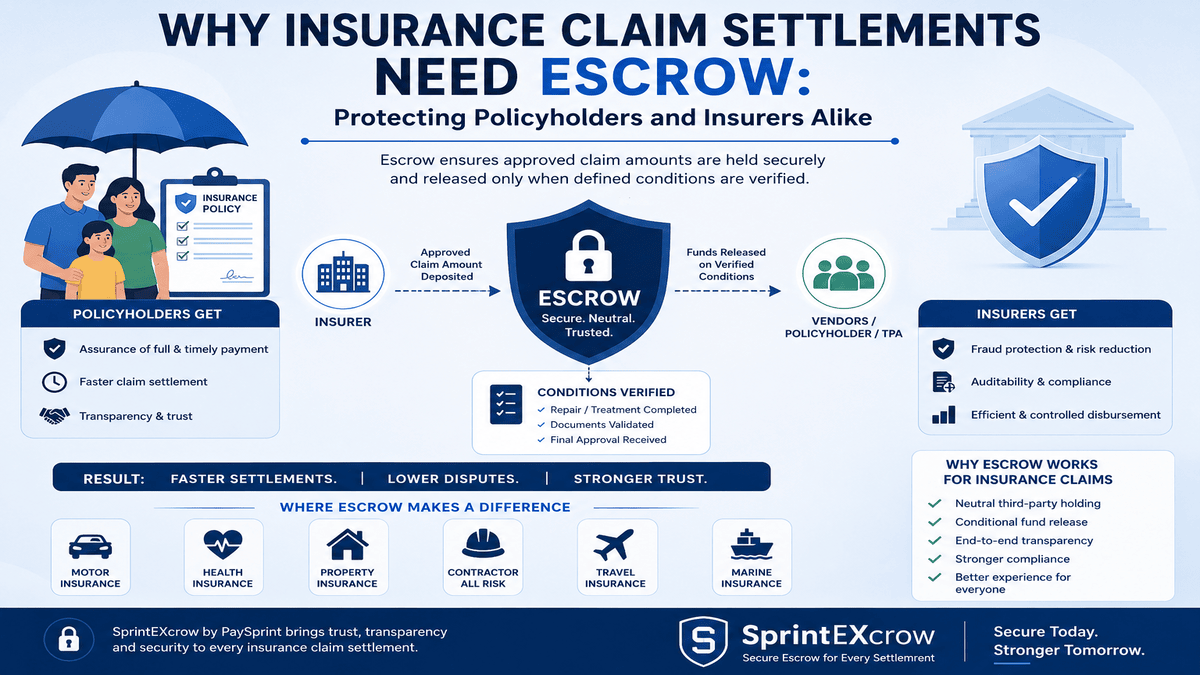

Escrow is a financial arrangement in which a neutral third party — the escrow agent — holds funds from one party and releases them to another only when pre-defined conditions are met. In an insurance context, those conditions are the verified completion of the obligation that the settlement is intended to fund.

Applied to insurance claim settlement, escrow works as follows:

1. The insurer approves a claim and deposits the approved settlement amount into a secure SprintEXcrow escrow account.

2. The policyholder, vendor, or TPA is notified that the approved funds are committed and held in escrow — giving all parties certainty that payment exists and is secured.

3. The defined release conditions are monitored — repair completion, hospital discharge, contractor invoice verification, or any other verifiable milestone.

4. When conditions are verified and confirmed, SprintEXcrow releases the funds to the designated party automatically.

5. If a dispute arises, funds remain in escrow until resolution — with a full audit trail available to all parties and, if necessary, to IRDAI or a court.

This single structural change converts insurance settlement from a trust exercise into a process exercise. The money is there. The conditions are clear. The release is automatic. The dispute resolution is documented.

How SprintEXcrow Works for Insurance Claim Settlement

SprintEXcrow by PaySprint is an enterprise-grade escrow platform that provides the legal, technical, and operational infrastructure for condition-based payment release at scale. For insurance organisations managing thousands of claim settlements simultaneously, the platform delivers:

Secure Fund Holding with Full Visibility

Approved claim amounts are held in audited, RBI-compliant escrow accounts with 24/7 access monitoring. Insurers retain visibility into every fund position. Policyholders can see that their approved settlement is committed and waiting.

Configurable Release Conditions

Release triggers are fully configurable to the specific settlement type: hospital discharge and final bill submission for health claims, repair completion certificate and inspection for motor claims, surveyor sign-off and contractor invoice for property claims. Any verifiable milestone can serve as a release condition.

Multi-Party Escrow Architecture

Insurance settlements frequently involve three or more parties — insurer, policyholder, TPA, and vendor. SprintEXcrow’s multi-party escrow structure supports controlled access and role-based visibility for each party, with funds released to the correct beneficiary based on the verified trigger.

Automated, Milestone-Based Payouts

For complex claims with phased settlements — ongoing medical treatment, staged property restoration, multi-year disability payouts — SprintEXcrow automates milestone-based fund release without requiring manual intervention at each stage.

Immutable Audit Trail

Every event in the settlement lifecycle — fund deposit, condition verification, release instruction, and disbursement confirmation — is recorded in a complete, timestamped audit trail. For IRDAI compliance, internal audit, or dispute resolution, the full history is available instantly.

SprintEXcrow’s multi-party escrow architecture is designed specifically for transactions involving three or more parties — making it the natural fit for insurance settlements where insurer, policyholder, TPA, and vendor must all operate within the same payment framework.

Who Benefits — Policyholders, Insurers, and TPAs?

Escrow in insurance claim settlement is not a benefit for one party at the expense of another. It restructures the payment process in a way that delivers measurable value to every stakeholder.

For Policyholders

The policyholder’s fundamental need is certainty: certainty that an approved claim will be paid in full, to the right party, within a defined timeframe. Escrow delivers this. Once the insurer deposits the approved amount, the policyholder has documentary confirmation that the funds are committed and cannot be retracted without a defined process.

For Insurers

Insurers benefit from reduced fraud exposure, lower dispute volumes, and stronger IRDAI compliance positioning. Condition-based release means funds are only disbursed when the underlying obligation has been verified — eliminating the most common vectors for claim fraud at the payment stage. The audit trail reduces the cost and complexity of dispute resolution.

For Third-Party Administrators (TPAs)

TPAs managing disbursements across large claim portfolios benefit from automated release workflows that reduce manual processing, eliminate reconciliation gaps, and provide real-time visibility into fund positions. SprintEXcrow’s platform integrates with TPA workflows via API, enabling escrow to operate at the volume TPAs require.

For Repair Vendors, Hospitals, and Contractors

Third-party service providers who perform work on the expectation of insurance reimbursement gain payment certainty before they begin — the escrowed funds confirm that approved payment exists, reducing the risk of performing services for which reimbursement is subsequently disputed or delayed.

Where Insurance Escrow Matters Most: Key Use Cases

Motor Insurance Claims

Motor claims are the highest volume insurance category in India. Escrow releases payment to the authorised repairer only upon verified completion of repairs and inspection sign-off — preventing both premature release and fraudulent inflation of repair invoices.

Health and Mediclaim Settlements

For cashless hospitalisation and reimbursement claims, escrow holds the approved amount and releases it to the hospital or policyholder upon verified discharge documentation and final bill submission. Disputed amounts remain in escrow while resolution is pursued — the patient’s treatment is not held hostage to the payment dispute.

Property and Fire Insurance Claims

Large property claims involving staged restoration work benefit from milestone-based escrow release tied to surveyor sign-offs at each stage — ensuring the contractor has certainty of payment while the insurer has assurance that work is progressing as agreed before funds are released.

Life Insurance and Annuity Payouts

For structured settlements, disability payouts, and annuity disbursements, SprintEXcrow manages time-based and condition-based release schedules — ensuring that long-duration payment obligations are fulfilled systematically with full audit visibility at each disbursement.

Disputed Claims in Litigation

When a claim is under litigation or IRDAI grievance review, escrow holds the undisputed quantum while the dispute is resolved. Neither party can access the disputed amount unilaterally — removing the incentive to delay resolution and providing courts or regulators with a clear picture of what is held and on what basis.

Why SprintEXcrow Is Built for Indian Insurance Settlement

IRDAI and RBI Regulatory Alignment

SprintEXcrow is designed in alignment with RBI Master Directions on IT Framework and operates within the regulatory parameters applicable to insurance payment intermediaries. The platform’s audit trail and fund segregation capabilities directly support IRDAI’s requirements for transparency and policyholder protection in claim settlements.

ISO 27001 Certified Security

All escrow funds and transaction data are protected by end-to-end encryption, 24/7 monitoring, and two-factor authentication. SprintEXcrow is ISO 27001 certified and undergoes VAPT by a CERT-In empaneled auditor — meeting the security standards expected by Indian insurance regulators and enterprise clients.

API Integration for Insurers and TPAs

SprintEXcrow’s platform integrates via API with insurer core systems and TPA claims management platforms, enabling escrow to operate within existing workflows without requiring a separate interface for settlement teams. Automated release triggers reduce manual intervention and processing time.

Scalability Across Claim Volumes

Indian general insurers process millions of claims annually. SprintEXcrow is built to handle high-volume, concurrent escrow arrangements — from a single motor claim to a portfolio of thousands of health claims managed simultaneously.

PaySprint’s broader ecosystem — including SprintVerify for policyholder KYC and identity verification, and SprintNXT for connected business banking — gives insurance organisations a complete trust and payment infrastructure stack from a single provider.

Conclusion

Insurance was built on a promise. The premium is the policyholder honouring their side of that promise. The settlement is the insurer honouring theirs. When the settlement process fails — delayed, disputed, diverted, or defrauded — the promise is broken, and the entire proposition of insurance loses credibility.

Escrow does not make the promise. It makes the promise enforceable. By holding approved claim funds in a neutral, conditional account and releasing them only when defined obligations are verified, SprintEXcrow converts the most fragile moment in the insurance lifecycle — the payment — into its most reliable one.

For policyholders, it is certainty that an approved settlement will be paid. For insurers, it is control, auditability, and fraud protection. For the Indian insurance industry, it is the infrastructure that makes claim settlement trustworthy at scale.

Frequently Asked Questions (FAQs)

Q: What is insurance claim escrow and how does it work?

Insurance claim escrow is an arrangement where the insurer deposits an approved settlement amount into a secure, neutral escrow account managed by SprintEXcrow. The funds are released to the policyholder, vendor, or TPA only when pre-defined conditions are met — such as repair completion, hospital discharge, or surveyor sign-off. If a dispute arises, funds remain held until resolution, with a full audit trail available to all parties.

Q: How does escrow protect the policyholder in a claim settlement?

Escrow gives the policyholder documentary certainty that an approved claim amount is committed and secured — the insurer cannot retract it without a defined process. Funds are released in full, to the correct party, when the agreed conditions are verified. The policyholder no longer depends on the insurer’s internal payment queue or goodwill to receive what they are owed.

Q: Can SprintEXcrow handle high-volume insurance claim disbursements?

Yes. SprintEXcrow is built for enterprise-scale volume and integrates via API with insurer core systems and TPA claims management platforms. Automated, milestone-triggered release workflows mean the platform can manage thousands of concurrent escrow arrangements without manual intervention at each disbursement step.

Q: Is SprintEXcrow compliant with IRDAI and RBI requirements?

SprintEXcrow is designed in alignment with RBI Master Directions on IT Framework, and its fund segregation, audit trail, and transparency capabilities directly support IRDAI’s policyholder protection requirements. The platform is ISO 27001 certified and undergoes VAPT by a CERT-In empaneled auditor.